Now I know it may sound a bit crazy. In fact I would probably give my dad a heart attack if I told him. But hear me out. Refinancing your home in order to invest may not be such a bad idea. In fact in some cases in might get you to financial independence sooner rather than later.

I decided to refinance my home in order to invest, but I did not take the decision lightly. I really dug into the numbers and decided that I could net more with a 3% dividend than I was paying out in bank interest. The dividend is a conservative estimate of my cash flow, I plan to at least match the historical market returns of 7-8%.

In order to refinance to invest you will need a cash out refinance. This means you will need to make sure you have enough equity built up in your home, in order to take some of the value out in the form of cash.

Home Equity Builds Over Time

I’ve owned my home for nearly eight years at the time of this writing. That’s a long time and indeed longer than most. I thought it was a mistake buying such a long time ago, but inflation and time works in the favor of the patient. The problem was I was house rich and cash poor during most of those eight years which really made it tough to invest.

Over those eight years my home doubled in value. This is because I bought really low in December of 2011. If you bought during a period of time where home values were high and the price had dropped than it may be a bit difficult to refinance, but not entirely out of the question.

Even if your home value is dropping in price you are still building equity in your home every month. This will slowly chip away at the principle.

Now after 8 years of appreciation, principle reduction and now unbelievably low interest rates it makes complete sense to tap into some of that home value in order to invest. But, it can be very dangerous so lets take a look at some reasons you may not want to do this.

- Your investing skills are not great.

- Your emotional temperament is not solid.

- You don’t trust yourself to use your refinance for only investing.

- You don’t have a lot of equity built up in your home.

Even though fixed home loans are considered good debt. It’s still dangerous to play around with, so unless you know that you can make the new payments every month and have an emergency fund its not recommended.

Why The Math Made Sense in My Situation

My previous home loan was 3.5%. This seemed extremely low at the time and I thought I would have that loan forever. Until 2020 happened. Then the home loans dropped to below 3%. This was crazy.

I was able to snag a home loan for about 2.67% after fees. In my situation not only was I able to get a lower interest rate and thus pay less money per month. I was also able to cash out some of my home equity in order to use it to invest. Not to mention I was able to pay off a car loan and immediately simplify my finances.

The reason this cash out refinance made sense to me is I could find cheap value stocks that not only were trading below net current asset value, but also paid out dividends more than 3%. This gave me the amazing opportunity to have a nearly risk free return at least in terms of cash flow.

These dividend trades are not entirely risk free because the companies could decide to cut their dividends. But, the best way to avoid this is to invest in cheap cash rich companies that will hang onto their dividends while they improve operations.

Now in order for investing a cash out refinance to be worth it you will need to actually invest this money for the long term, and I mean long term. Upwards of 4 years in order to get your money’s worth through a boom and bust cycle. It could be sooner, but be prepared for the long haul.

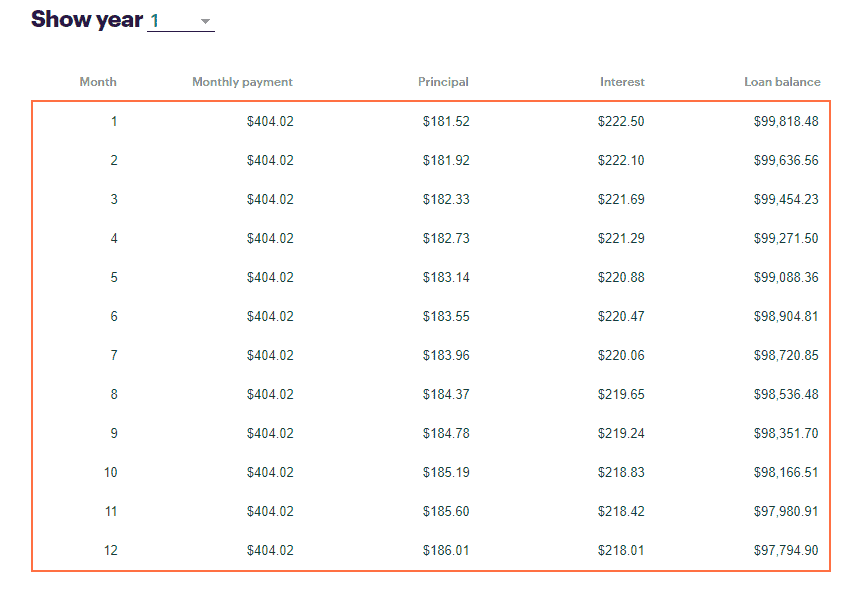

Amortization Schedule and Dividend Investing

If you were not quite sure why the math makes sense when investing in dividends behold the amortization schedule.

If I invest the entirety of the 100,000 dollars that was pulled out of the home and made sure that I only invested in stocks that had over a 3% dividend I would be netting an extra $27.50. The best part is that the amount of profit that I would make increases every month for the longer I hold the loan.

Dividend yields are annualized so $100,000 at 3% equals $3,000. Divide that by 12 and you have $250 per month.

It’s important to note that that dividends are not paid out on a monthly basis so you will need to have cash reserves to cover a loan like this but that math is simply crazy. Not to mention the potential for capital appreciation given enough time.

You Don’t Have to Invest in Stocks

When doing a cash out refinance you don’t have to invest in stocks. In fact many even start up their own businesses with the proceeds. Although in my opinion this is probably more dangerous than investing, since new businesses often fail at high rates.

Another great investment and one that might even net you higher returns over time than the stock market would be to buy an income producing blog.

Blogs will often sell for their revenue times 36 months. This means in 3 years you will theoretically make back your investment. However, it’s important to know what you are doing and in some cases you may even be able to increase that revenue to make back your money even faster.

Tax Deductions and Capital Gains

I don’t make a lot of money, but I am house rich so refinancing in order to increase my stock exposure and reduce the amount of capital tied up in my house makes a lot of sense. The problem is tax deductions don’t exactly work in my favor. This is because I can’t get past the standard deduction.

However, this is a net benefit when it comes to capital gains. Since Selling off stocks at a profit won’t push me into a high enough tax bracket for it to hurt my dividends and stock gains more than the difference in the interest rate.

Why You Should Not Refinance to Invest

The whole process of refinancing to invest is a bit frustrating. In fact I thought I was going to make an extra 1000 dollars but because the refinancing took so incredibly long I missed out on easy money. It has taken 4 months for my refinance to complete and because of that I lost the opportunity to get some dividends.

The was beyond frustrating but entirely out of my control. So just make sure if you do decide to invest your cash out refinance you take into account anything that may go wrong. My situation hurt more than usual because many of the high dividend stocks I wanted to invest in were Japanese and only had payouts once per year.

So to say the least a large portion of my short term benefits of investing went up in flames. Now all I have to look forward to is my long term investments. If you want to learn more about investing be sure to follow along on my blog as I Exploit Investing. Also follow me on Seeking Alpha to see some of my trades in the United States.